Have you ever wondered how an economy works? And how do even our smallest economic activities play a vital role in its development? If you’re curious about how an economy works, this article is for you, and it will transform your perspective on the economy.

The data, structure, and state of the local, national, and global economy are always in the news because people, institutions, and businesses rely on them to make future economic and business decisions. But how? Because they understand the principles and systems under which the economy operates.

Without understanding how an economy works, you can’t make sound financial decisions. No matter who you are—an employee, a trader, an investor, a businessman, or a common man—it’s important to understand how an economy works where you live.

Here, we will understand the basic principles of the economy, how different decisions affect it, and how to apply these principles to make good financial decisions.

Understanding How an Economy Works and Why It Truly Matters

Understanding how an economy works isn’t just about academic knowledge or statistical data from a region or country. The economy is a living, dynamic system that operates every second, like compounding.

Every single day, you participate in the economy, whether you realise it or not. But you are shaping the economy through your economic and financial activities. When you buy coffee (it can be anything), receive your salary, pay rent, invest in stocks and assets, take out a loan, or scroll through advertising-laden social media apps, you are part of an economic system.

To truly understand how an economy works, we must first understand that the economy is a network of people’s decisions. It is a living, dynamic network of decisions, production, consumption, money flow, credit, trust, and expectations.

Every person makes decisions for their own benefit. Every business makes decisions for profit. Governments make decisions for national stability and growth. All these decisions connect and influence each other, forming an ecosystem called the economy.

What is an Economy?

An economy is a system through which individuals and businesses in society produce, distribute, and consume goods and services. An economy is formed when people work together, using their unique skills, talents, and resources to create goods and services and trade them with others. Whenever people exchange goods or services in the hope of receiving something valuable, a market automatically forms. Over time, these countless transactions form the foundation of what we call an economy.

Every person, business, community, and country faces the same basic truth: people want more than what exists. We want better homes, better healthcare, better technology, more things to live comfortably, more security, and more convenience.

However, land is limited. Natural resources are limited. Skilled labour is limited. Time is limited. But our needs are unlimited. Because resources are scarce, societies must make choices. These choices determine how an economy works.

For example, consider your country, which has limited land. That land can be used for agriculture, factories, homes, or infrastructure. It can’t be used for everything at once. Decisions must be made about allocation. These allocation decisions are the foundation of the economy. Simply put, an economy works by allocating scarce resources in a way that satisfies human needs and desires.

Important key terminologies of the economy

To make better economic and financial decisions, understand these key terminologies used to describe or analyse the economy. These terms will help you to understand how an economy works.

Gross Domestic Product (GDP): Gross domestic product measures the total monetary value of all final goods and services produced within a country’s borders over a specific period of time, usually a year.

Inflation: Inflation refers to the steady increase in the general price of goods and services over time. When inflation increases, the purchasing power of money decreases. It is a silent killer that erodes the value of your money over time.

Deflation: Deflation is a decrease in the general price level of goods and services. Although lower prices may seem beneficial, long-term deflation can reduce business profits, salaries, and jobs, slowing economic activity.

Unemployment: Unemployment occurs when people willing and able to work cannot find jobs. High unemployment often signals economic weakness and underutilised resources.

Demand: Demand is the willingness and ability of consumers to purchase goods and services at a given price. It depends not only on willingness but also on purchasing power and other factors.

Supply: Supply represents the quantity of a good or service that producers are willing and able to supply at different prices. Higher prices generally lead to greater supply.

Market: A market is a system or platform where buyers and sellers negotiate to exchange goods, services, or financial assets. Prices are generally determined by the forces of demand and supply in every market.

Capital: Capital refers to human-made resources, such as machinery, tools, technology, and financial assets, that are used in the production of goods and services. It increases efficiency, productivity, and economic output.

Labour: Labour represents human effort—both physical and mental—used in the production process. It is one of the fundamental factors of production in any economy.

Entrepreneurship: Entrepreneurship is the ability and willingness to organise resources, take risks, and create new businesses. Entrepreneurs create jobs and promote economic growth.

Fiscal Policy: Fiscal policy includes government decisions related to taxes, regulations, and public spending. It is used to manage economic growth, control inflation, and reduce unemployment.

Monetary Policy: Monetary policy refers to the measures a country’s central bank takes to control the money supply and interest rates. This helps stabilise inflation, manage liquidity, and support economic growth.

Recession: A recession is a significant, prolonged decline in economic activity. It is often characterised by falling GDP, rising unemployment, and reduced consumer spending.

Economic Growth: Economic growth refers to the increase in the production of goods and services in a country over time. It is usually measured by GDP growth and reflects a better standard of living.

Scarcity: Scarcity is a fundamental economic problem in which human wants are unlimited, but resources are limited. This forces society to choose how resources are distributed.

Stock Market: The stock market is a platform where individuals and firms can buy and sell, or trade, publicly listed securities. It includes the buying and selling of stocks, mutual funds, ETFs, and bonds.

Things and scenarios that play an important role in building a better economy

Many scenarios and factors play a vital role in economic growth and become growth drivers for the economy. These interconnections create and sustain a better economy.

1. Starting Point of an Economy: Human Needs and Scarcity of Resources

Scarcity is the primary reason for economies. If Earth’s resources were unlimited, there would be no need for pricing, markets, economic systems, or hard work.

Because there is scarcity, every economy, even every market, must answer three key questions:

What should be produced?

How should it be produced?

For whom should it be produced?

These are not just theoretical questions. These are real, everyday decisions.

For example, a government deciding whether to build government offices or highways is answering the question of what should be produced. A company choosing between manual labour and automated robots is deciding how production should take place. The pricing of goods determines who can buy them, which in turn determines whose production is for.

Human needs are unlimited. We want more than is available, which creates scarcity, which shows that the economy is really about trade-offs. Producing more of one thing means producing less of another.

The Factors of Production:

To create anything in any economy, four essential inputs must come together: natural resources, human effort, capital, tools, and entrepreneurship.

Natural resources include land, water, minerals, oil, forests, and all raw materials from nature.

Labour represents human effort, both physical and intellectual. Engineers, farmers, factory workers, doctors, teachers, and software developers all contribute labour to the economic system.

Capital refers to human-made tools that aid production. Machines, factories, vehicles, computers, and technology all fall into this category.

Entrepreneurs are people who take risks, organise the other three factors, and make decisions about production and pricing.

Each stage involves the coordination of the four factors of production. Without this coordination, modern economies cannot function.

Demand and Supply of Goods and Services:

To understand how an economy works, you need to understand that ,Markets are driven by the forces of demand and supply. Prices are not determined randomly; they emerge from the interactions between buyers and sellers.

Whenever demand for a product increases while supply remains the same, prices tend to rise. Higher prices signal to producers that the product is profitable, encouraging them to increase production. As supply increases, prices stabilise.

For example, when remote work increased worldwide, demand for laptops and home office equipment increased rapidly. Manufacturers responded by increasing production capacity. Over time, the market adjusts.

This decentralised coordination through price signals is one of the most powerful aspects of how an economy functions. No central authority or individual needs to dictate every production decision; the market decides through prices.

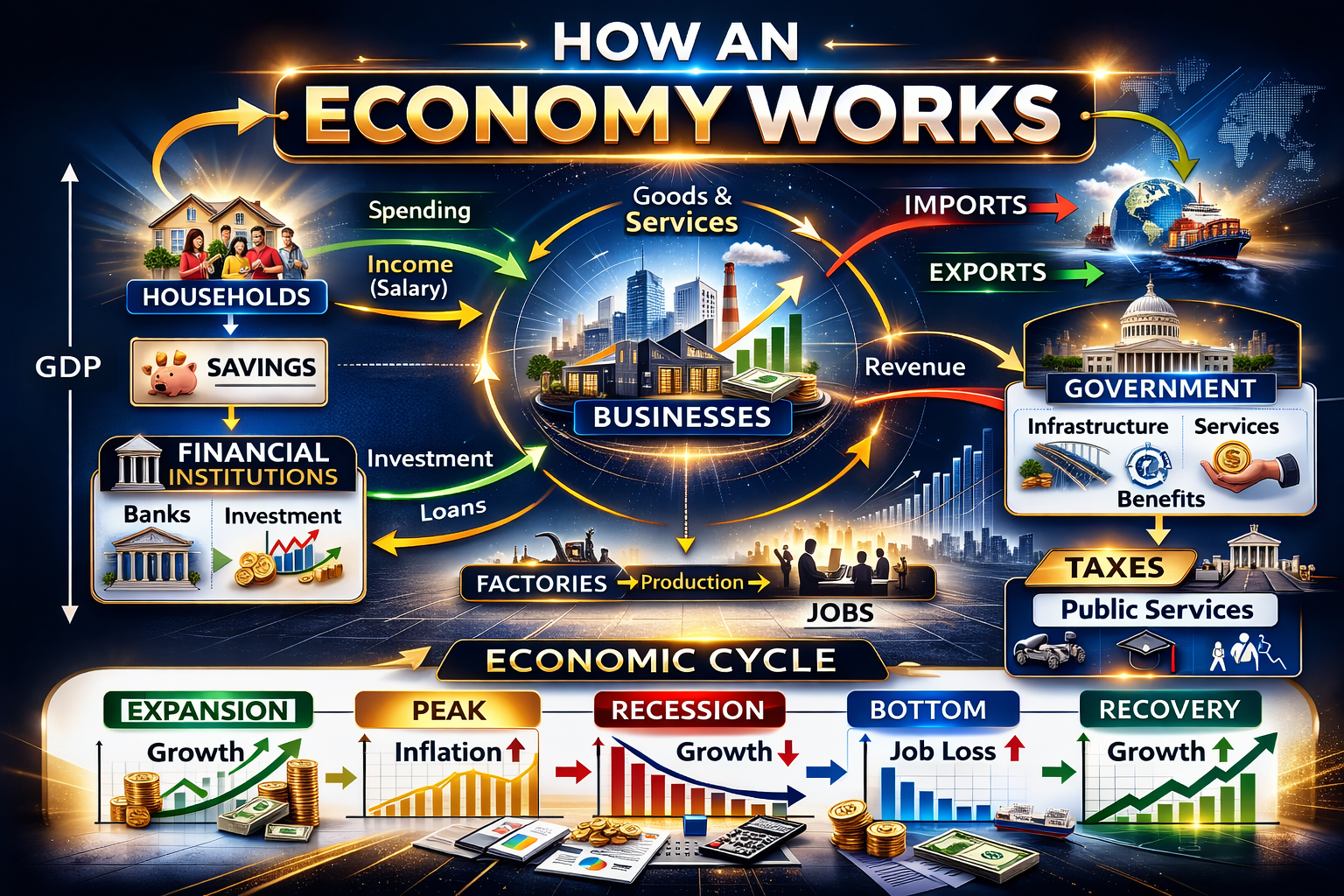

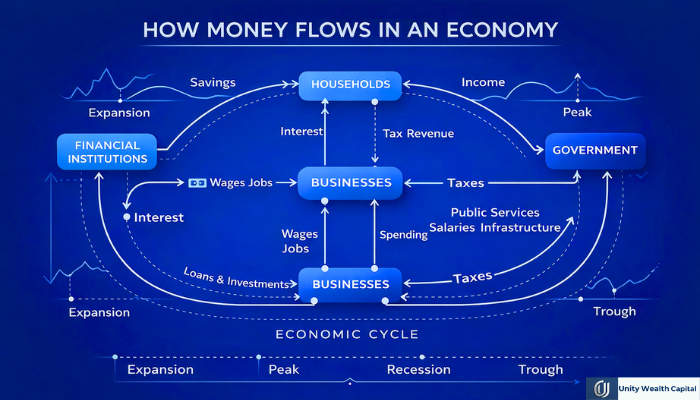

The Circular Flow of Income: How Money Moves in economy

The clearest way to understand how an economy works is through the circular flow of income, i.e., how money circulates through the economy.

Households provide labour and other resources to businesses. In return, businesses pay wages, salaries, rent, and profits. Households then use that income to buy goods and services that are produced by businesses. This expenditure becomes revenue for businesses. That revenue allows businesses to continue paying wages, salries and investing in expansion.

This creates a never-ending and continuous loop of income and expenditure. If households suddenly reduce spending, businesses earn less revenue. Lower revenue may force companies to reduce hiring or lower wages. Lower income further reduces spending. This downward cycle can lead to a recession.

On the other hand, when incomes rise and consumer confidence strengthens, they spend more. Businesses increase production due to high demand, hire more workers, and invest in growth. This upward cycle fuels economic growth.

This dynamic interaction between production, income, and spending is crucial to understanding how an economy works.

Role of Consumer and Businesses: Engines of Production and Expenditure

Consumers use the products and services that are produced by businesses. They spend a significant portion of their income on their needs and wants. Consumers create demand for goods and services, which shapes businesses and industries.

When incomes rise, people’s confidence in the economy increases, they change their lifestyles, and therefore, they spend more and invest more. This process accelerates the economy and leads to growth.

Businesses are the main producers of goods and services in the market. They convert inputs into outputs and create value in the process.

Businesses also create employment. Employment generates income. Income drives consumption. Consumption sustains businesses. This interdependence again demonstrates how an economy functions through interconnected relationships.

Businesses drive innovation. Technological advancements, efficiency improvements, and new products often come from profit-seeking private companies.

For example, technological innovation in the United States has significantly shaped the global digital economy. Meanwhile, massive manufacturing capabilities in China have transformed global supply chains.

Role of Governments and Banks: Stabilizing economy and controlling inflation

Governments play a vital role in ensuring stability, fairness, and infrastructure development.

Governments collect taxes and use them to fund public goods such as roads, infrastructure, education, healthcare, defence, and law enforcement. Governments also regulate industries to prevent monopolies and ensure consumer protection.

Furthermore, governments use fiscal policy by adjusting spending and taxes to influence people to engage in economic activity during periods of economic slowdown or overheating.

Modern economies rely on monetary systems managed by the country’s central bank. Central banks control interest rates and the money supply to maintain economic stability.

When inflation rises too rapidly, central banks raise interest rates. Higher interest rates reduce borrowing and spending, slowing economic activity. When growth slows significantly, they lower interest rates to encourage borrowing and investment.

And commercial banks act as financial intermediaries. When people deposit money, banks lend a portion of those deposits to businesses and consumers.

A business might borrow to expand a factory. A family might borrow to buy a home. These loans generate economic activity. Construction companies get contracts. Suppliers supply goods. Workers get wages. Spending increases.

Example: Understand how an economy works with a master example:

Let’s understand how an economy works with an example that connects each of the key components of the economy.

The Income Cycle Begins

Let’s say Rohit works at an AMC (Asset Management Company). He receives a salary of ₹80,000 at the end of the month.

The question is: where did this ₹80,000 come from?

The company provided services to clients. Clients paid the company. The company gave a portion of that money to Rohit as salary.

Customer → Company → Employee

Money flows through expenses.

Now Rohit takes his salary home, and he starts spending. He pays rent, buys groceries, recharges his internet, buys other things, and fills up on petrol.

Now Rohit’s ₹80,000 has gone to different people.

Employee → Shopkeeper → Distributor → Transport Company → Worker

The same money passes through many hands.

Businesses reuse that money.

Now the grocery store owner earned ₹5,000 from Rohit.

What will he do?

He will pay his supplier. He will pay his staff. He will pay the electricity bill. He will keep a small profit.

The supplier will give the money to the truck driver.

The truck driver will give it to the petrol pump.

The petrol pump owner will give it to the oil company.

Money doesn’t just sit there.

It keeps moving from one hand to another. Savings and investments come into the system.

Rohit saves ₹10,000 of his salary in the bank.

The bank gives a loan to someone else—let’s say Jack, who wants to open a grocery store.

Now Rohit’s savings are invested in Jack’s business.

Jack rents a shop and hires staff. Now, new people start receiving income.

Savings → Investment → New Income

This cycle continues to grow.

The government also gets involved in this flow.

Rohit pays taxes on his salary, and the grocery store also pays GST.

All businesses pay taxes to the government. The government collects money from all of them.

What does the government do now?

Builds roads. Operates hospitals. Pays salaries to police. Pays salaries to teachers.

The money collected by the government is returned to the public in the form of salaries and services.

Taxes → Government → Public spending → People’s income

Money returns to the market.

Expansion and Growth

Zack’s grocery store becomes popular. People start buying more. Zack opens another branch.

New employees are hired for the business. New rent is paid. New suppliers are added.

A small business now becomes a source of income for others. And the new employees hired speed up their spending cycle.

Slowdown Phase

Now, suppose people reduce their spending for some reason.

Rohit becomes cautious. He eats out less and spends less.

Due to lower demand, the grocery store’s sales drop slightly.

Zack no longer hires new staff, so he stops expanding the store.

The cycle slows down slightly.

This is the natural rhythm of the economy—sometimes fast, sometimes slow.

The Real Secret: Why It Never Stops

Now understand the most important thing: the economy is not a machine that stays still. The economy is a continuous circular movement in which:

People earn income, they spend it, and their spending creates income for others. Some money is saved. That money creates businesses, Businesses create new income, the government collects it and distributes it among itself.

And then the cycle repeats.

Why is this cycle powerful?

If Rohit doesn’t take a salary, if he doesn’t spend, the grocery store will earn less, the supplier will earn less, and the truck driver will earn less. One person’s decision affects others.

This interconnected flow is what we call the economy.

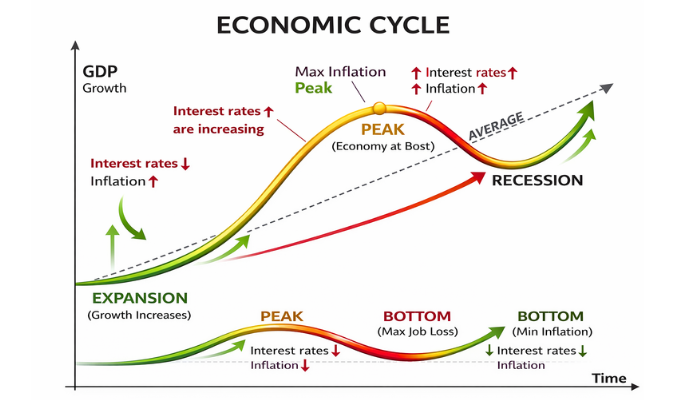

Economic Cycles: How it effect the economy?

The economic cycle, also known as the business cycle, reflects the natural ups and downs of the economy. The economy never, and cannot, grow in a straight line. It moves in a rhythm—sometimes fast, sometimes slow, sometimes falling, then rising again.

This movement doesn’t happen randomly. It’s driven by interconnected factors like spending, income, confidence, investment demand and supply, and the financial system.

Let’s understand this logically, step by step.

1. Expansion Phase – When the Economy is Growing

The expansion phase is a period when economic activity is increasing.

In this phase, companies are earning more. People are getting jobs. They became confident and spent more. Businesses start new projects, hire new employees, and plan their expansion.

In this stage, GDP grows, unemployment decreases, profits increase, and stock markets generally strengthen.

2. Peak – This is the point when growth is at its highest point.

Not every expansion continues indefinitely. There comes a time when growth reaches its maximum level. This stage is called the peak.

Prices begin to rise rapidly. Businesses become overconfident. People begin to borrow more. Asset prices rise.

Risk is increasing here, but everyone thinks everything is fine.

A peak is usually followed by a slowdown/recession.

3. Contraction (Recession) – When the economy begins to slow.

In this stage, growth begins to stagnate and then decline.

People become cautious. They reduce spending. They think everything is over. Business revenues fall. Companies stop expansion. Hiring slows.

This creates a negative loop.

If the slowdown becomes significant, it’s called a recession. For a historical example, consider the 2008 Global Financial Crisis.

During this time, the banking system collapsed, businesses closed, unemployment rose sharply, and the global economy shrank.

4. Trough – The Lowest Point

The trough is the second stage when economic activity is at its lowest point, the peak of a recession.

Unemployment rates are high.

Confidence is low. Investment almost stops, and no one talks about it.

But interestingly, recovery begins from this point.

Why?

Because prices have become relatively stable. Costs have adjusted. Governments and central banks provide support through their policies. Confidence gradually returns.

5. Recovery – The Cycle Begins Again

In the recovery phase, the economy gradually improves.

Businesses invest cautiously, and hiring begins.

Income begins to rise, and spending gradually increases.

Confidence returns among people.

And then the economy enters the expansion phase again.

The cycle is complete.

The same process repeats—expansion → peak → contraction → trough → recovery → expansion.

Why Economic Cycles Occur

Economic cycles are natural because:

Human emotions (fear and greed) fluctuate, which is the basis on which most people make their financial decisions. Spending and borrowing patterns change.

The financial system sometimes overheats. External shocks occur (war, pandemic, crisis).

For example: COVID-19 recession.

Lockdowns during the pandemic disrupted both spending and production. The economy contracted sharply. Stimulus and reopening then led to a recovery. Every recession holds opportunities for wealth creation.

The Connection Between Economic Cycle and Money Flow

Remember the example of circular money flow we discussed? The economic cycle is essentially a speed control of that flow.

Expansion = money is circulating faster in the economy.

Recession = money is circulating more slowly in the economy.

When people spend more, invest in businesses and financial securities, and borrow more, the economy accelerates.

When people save more and spend less for any reason, money circulation in the economy slows down.

The cycle is essentially a pattern of the speed of money flow.

The Conclusion

Today, we understands how an economy works. The economy isn’t just a system of markets, money, or business. It’s a living, constantly moving network of people making decisions every day. People earn money, but money doesn’t stay in one place; it circulates throughout the economy, creating opportunities, jobs, and growth.

The economic cycle reminds us that both growth and slowdown are natural. Growth periods bring hope, rising incomes, and new investments, while contractions bring caution, adjustments, and corrections. No phase is permanent. The economy moves like waves, just as nature responds to the seasons.

Understanding how an economy works changes our perspective on the world. It helps us remain calm during downturns, make better financial decisions, and recognize opportunities during recessions and recoveries. The economy is not something separate from us—we are the economy, we create it. Our decisions shape it, and in turn, it shapes our financial future.