In the world of investing and corporate finance, Enterprise Value is a financial metric that evaluates the actual value of a company. Most investors only look at a company’s market capitalisation to determine a company’s value; this is only one part of the whole picture. Enterprise value reflects a more realistic valuation of a company than market capitalisation. It includes not only the price of a company’s shares, but also its debts, cash reserves, and other financial obligations or assets.

What is Enterprise Value (EV)?

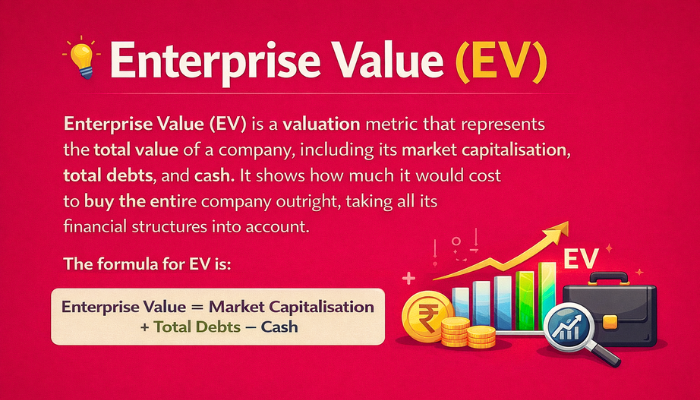

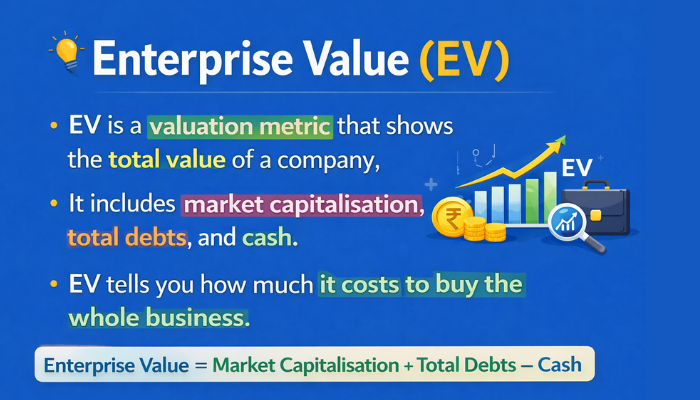

Enterprise value (EV) is a financial measurement tool used by investors to determine the actual value of a company’s total assets. Its calculation not only includes the company’s market capitalisation, but it also includes both long-term and short-term debt, cash, and cash equivalents, which are listed on the company’s balance sheet. This is a more comprehensive valuation method than market capitalisation.

How does Enterprise Value (EV) work? :

Enterprise value is slightly different from simple market capitalisation in several ways, such as:

It tells investors the most accurate value of the total company. Enterprise value tells investors or interested buyers the actual value of the total company, i.e. how much money you would need if you wanted to buy the entire company. Meaning, after paying off all those loans/debts, how much is that company worth to you? This is called Enterprise Value.

A company’s EV can be negative if the total value of its cash and cash equivalents is greater than the combined total of its market cap and debts. Negative EV is a sign that the company is not using its assets very well – it has too much cash lying around that is not being used.

A negative EV does not always mean a bad company. In some cases, it indicates a strong balance sheet where the company holds a significant portion of cash reserves and maintains minimal debt. These types of situations are often seen in cash-rich technology firms or companies that have recently sold assets but have not yet reinvested the cash. You can find undervalued stocks from the enterprise value of the company compared with that of its peers.

Components of Enterprise Value:

The components that make up Enterprise value :

- Equity: Equity represents shareholders’ initial investment, calculated based on the number of outstanding shares fully diluted to the current price per share. fully-diluted means they are inclusive of warrants, convertible securities and basic shares outstanding.

At the time of acquisition, the acquirer must pay at least the market capitalisation to its shareholders. However, market capitalisation alone does not cover the actual and total value of the company. Other factors, such as debt, cash, preferred stock, and non-controlling interest, are also considered in calculating EV.

- Debt: Total debt means the sum amount of short-term or long-term debt that reflects the company’s obligations towards financial institutions and their creditors. Cash is deducted from total debt when the enterprise value is calculated, as it reduces the cost of acquisition. The book value of debt is used in case its market value is unknown.

- Preferred stocks: Preferred stocks are hybrid securities that blend features of debt and equity. Preferred stocks are treated like debt as a component of enterprise value because they pay a fixed amount of dividends and are considered more prioritised in terms of assets and earnings than common stocks.

- Minority Interest: If a company owns more than 50% but less than 100% of another company, the remaining part is considered a minority interest. The minority interest is added in the calculation of EV because the parent company includes the total revenue earned, expenses incurred and cash flow generated in its financial numbers.

- Cash and cash equivalents: Cash and cash equivalents means the total amount of cash, drafts, money orders, marketable securities, money market funds, short-term government bonds, or treasury bills, etc. These are subtracted from the total debt in calculating EV. Buyers use cash to pay off debt.

Formula and Calculation of EV :

Enterprise value is calculated by the sum of a company’s market capitalisation and debts, minus cash and cash equivalents on hand.

Enterprise Value = Market capitalisation + total Debts – cash

HERE :

Market capitalisation: total number of outstanding shares * current price per share

Total debts: the sum of both long-term and short-term debts.

Cash: sum of cash and cash equivalents

To calculate EV, = Firstly calculate the market capitalisation by multiplying the number of current shares outstanding by the price per share, and add the total debts of the company – amount of long-term or short-term debt. Then, subtract the cash and cash equivalents from the balance sheet of the company.

Example:

Let’s calculate enterprise value with the help of an example of a company, namely ABC Ltd.

| 1. | # Outstanding Shares | 50cr | |

| 2. | Latest Share Price | 100 | |

| 3. | Market capitalisation | 5000cr | Item 1*2 |

| 4. | Short-term debt | 00 | |

| 5. | Long-term debt | 1000cr | |

| 6. | Total Debt | 1000cr | Item 4+5 |

| 7. | Cash and cash equivalents | 1500cr | |

| Enterprise value | 4500cr | 3+6-7 |

Here, we can calculate the EV from the given information. Company ABC Ltd has 50cr outstanding shares valued at 100rupees per share.

- Market capitalisation of ABC Ltd is 5000cr ( 50cr*100)

- Total debt is 1000cr ( 0 +1000cr)

- Cash and cash equivalents (1500cr)

Enterprise value = 5000cr + 1000cr – 1500cr = 4500cr

Compare Market Capitalisation vs Enterprise Value with a simple Example

Let’s say two companies operate in the same industry – Company A and Company B

After analysing their balance sheet and income statement, we gathered some data to compare them based on EV.

| Names | Market capitalisation (cr) | Total Debt (cr) | Cash and cash equivalents (cr) |

| Co. A | 50,000 | 16,800 | 2,500 |

| Co. B | 46,000 | 750 | 4,500 |

EV of Co. A = 50,000cr + 16,800cr – 2500cr = 64,300 cr

EV of Co. A = 46, 000cr + 750cr – 4500cr = 42,250 cr

Although both companies appear approximately equally valued based on their market capitalisation, their enterprise values differ significantly.

Company A has an EV of ₹64,300 crore, while Company B’s EV is 42,250 crore. This is the real value of both companies.

This example shows why EV provides a more realistic picture of a company’s true valuation.

Financial Ratios: That Use Enterprise Value

Enterprise value isn’t just a standalone number—it’s the basis for several powerful financial ratios that investors and analysts use to evaluate a company’s performance, efficiency, and valuation. These ratios are especially useful when comparing companies with different capital structures or ratios. It relates the total value of a company from all sources to the earnings before interest, taxes, depreciation, and amortisation (EBITDA).

EV/EBITDA Ratio (Enterprise Value to EBITDA) :

The enterprise multiple (EV/EBITDA) metric is used as a financial valuation tool to compare a company’s value and its debt to the company’s cash earnings, minus its non-cash expenses. As a result, it is ideal for analysts and investors who want to compare companies within the same industry.

Formula :

EV/EBITDA = EV / EBITDA

A lower EV/EBITDA ratio tells us that the company’s stock is undervalued, which makes it an investment opportunity. A higher enterprise multiple suggests that the company is overvalued.

EV/EBITDA is especially useful for comparing capital-intensive businesses such as telecom, utilities, infrastructure, and manufacturing companies, where debt plays a significant role in operations.

EV/Sales Ratio :

The EV/sales multiple is another financial measurement tool used by investors to determine a company’s value from its revenue and sales. The EV/sales ratio is a more accurate measurement than the price/sales ratio because it considers the value and amount of debt that the company must repay at some point.

EV/Sales: EV / annual sales

A low EV/Sales multiple indicates that the company is undervalued relative to its revenue, which makes it more attractive. The EV/Sales ratio can be negative when the cash a company has is greater than its market capitalisation and debt value. A negative EV/Sales means that the company can pay off all of its debts.

Significance of Enterprise Value :

Enterprise value is a crucial financial metric used by investors to find out the real worth of a company. Here`s How :

- Enterprise value enables business entities or investors to find out the actual value of the target company.

- It provides a complete overall value of the economic worth of a company.

- This allows for a more ideal or accurate comparison of companies from different sectors or with different financial structures.

- The enterprise value comes with the fluctuations in the stock, which helps in calculating the estimated returns more effectively.

- EV reflects the theoretical acquisition price of the company to be paid by the acquirer and accounts for debts and cash that the acquirer will pocket.

Market capitalisation is a key component of enterprise value; it may be of limited utility for companies that are not listed or have limited share trading.

The conclusion :

Enterprise value is a financial metric that measures the actual value of a company. This means that if you buy the entire company, enterprise value tells you how much the company is actually worth. Enterprise value is not just for large institutions or investment banks; whether you are a retail investor, analyst or student of finance, you can use this tool to enhance your stock research.

Enterprise value is not like market capitalization which only shows how much a shareholder owns. It shows the real picture – the entire financial picture minus the debt or cash. It tells you how much you would actually pay to own the business, debt and everything.

Analyse enterprise value against other financial metrics such as cash flow, debt levels, EBITDA or sales to get a more accurate valuation.

Frequently Asked Questions

Why is Enterprise Value better than Market Capitalisation?

Enterprise value is better because it considers the entire financial structure of a company, including debt and cash. Market capitalisation only reflects the value of equity, whereas EV shows the real cost of acquiring the business.

Is a low Enterprise Value always good?

Not always. A low enterprise value may indicate undervaluation, but it could also reflect poor business performance, declining revenue, or weak prospects.

Which industries rely most on Enterprise Value?

Enterprise value is widely used in capital-intensive industries such as banking, telecom, energy, infrastructure, and manufacturing, where debt plays a major role in the operations.

Can Enterprise Value be negative?

Yes, enterprise value can be negative when a company’s cash and cash equivalents exceed its market capitalisation and total debt. This usually indicates excess cash on the balance sheet.

Should retail investors use Enterprise Value?

Retail investors can use enterprise value along with ratios like EV/EBITDA and EV/Sales to make more informed investment decisions and avoid misleading valuations.