In the world of finance and investing, nearly every investor invests in ETFs as a passive investment. When researching passive investments, two terms frequently come up: ETFs and index funds. If you’ve ever been confused about which one to choose, you’re not alone. Many investors search for “the difference between ETFs and index funds” because they appear nearly identical.

Both track the same index. Both offer diversification. Both are considered “passive” investments. So what’s the real difference between them?

Here, we’ll explain everything you need to know about ETFs and index funds. You’ll understand exactly how they differ, which one is right for your specific situation, and how to make your first investment with confidence..

Understanding Index Funds And ETFs

Before we dive into a direct comparison between ETFs and index funds, let’s first clarify the basics. Because if you don’t understand what these things are, there’s no point in comparing them.

What is an index fund?

An index fund is a type of mutual fund designed to track a specific stock market index (it can be small-cap, large-cap, or sector-specific). Simply put, it’s a fund that replicates what an index does.

For example, if you invest in an index fund that tracks the Nifty 50, your fund will hold the same 50 companies as the Nifty 50 index.

Here, the fund manager’s of these funds job isn’t to beat the market or pick winning stocks. Their job is simply to follow and match the index as closely as possible.

This sounds trivial, but in reality, research shows that over 80% of active fund managers find it difficult to beat the market over the long term. Therefore, it’s better to pay higher fees for active management, which typically underperforms, rather than paying lower fees simply to match the market. Even our legendary investor, Warren Buffett, says that index funds are better than active

What Exactly Are ETFs?

An ETF, or Exchange-Traded Fund, is also designed to track an index or mutual funds. But here’s the key difference: ETFs trade on stock exchanges just like regular stocks, like SBi or HDFC bank.

ETFs can have expensive and cheap management fees, according to their types.

Example: You want to invest $10,000 in the Nifty 50. Instead of buying an index fund, you buy an ETF that tracks the Nifty 50. This ETF also holds the same 50 companies in the same proportions. Your returns will be almost identical to the index fund version.

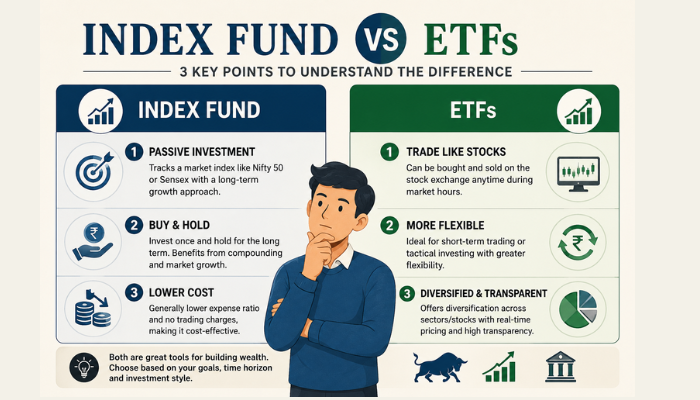

The Core Differences Between ETFs and Index Funds

Now that we understand what each one is, let’s break down the specific differences that actually matter to you as an investor.

The Core Differences Between ETFs and Index Funds

Trading Flexibility

You cannot buy an index fund at any time. Index funds can only be bought or sold once per day, after the market closes. When you place an order to buy an index fund at 2 PM, your order doesn’t execute immediately. It executes at the end of the day at the closing NAV price. So, you won’t know the exact price until after the market closes.

ETFs trade through a stock exchange just like stocks. If you place a market order at 1 PM, it executes immediately at the current market price. You know exactly what price you’re paying before you confirm the purchase.

But if you want to execute trades at specific prices, ETFs give you that flexibility rather than index funds.

Expense Ratios and Costs

Both ETFs and index funds are known for low costs compared to actively managed funds. But there are subtle differences. Index funds charge an expense ratio, which is automatically deducted from your returns.

ETFs also charge expense ratios, and many ETFs actually have lower expense ratios than comparable index funds. You can find ETFs with expense ratios as low as 0.03% to 0.10%. But Frequently buying and selling ETFs can increase your expenses.

For most investors investing in popular, low-cost funds, the total cost difference is minimal. But it’s something to be aware of.

Minimum Investment Amounts

Index funds often have minimum investment requirements. But ETFs have no minimum beyond the price of one share. If an ETF costs ₹150 per share, that’s your minimum investment. Investors with limited capital generally have lower barriers to entry with ETFs. You can start investing with whatever amount you have available for investing.

Differences between Index Funds And ETFs

| Factor | Index Funds | ETFs |

| Trading | Only Bought/sold once per day at closing NAV price after market closes; exact price unknown until day ends. | It trades throughout the day like a common stock; market orders execute immediately at the known current Bid/Ask price |

| Minimum Investment | Often require ₹500-₹10,000 minimum (varies by fund company) | No minimum criteria beyond one share’s price. You can buy a share. |

| Expense Ratio | Generally Low, automatically deducted from returns. | ETFs often have even lower expense ratios (0.03%-0.10%), but may involve brokerage commissions and bid-ask spreads. |

| Tax Efficiency | Less efficient — when the fund sells holdings, capital gains get distributed to all shareholders (even if you didn’t sell) | More tax-efficient due to “in-kind redemptions,” which avoid triggering capital gains distributions |

| Re-Investments | Very easy — set a fixed dollar amount monthly, buys fractional shares automatically | More complicated — purchases buy whole shares, so exact dollar-amount investing isn’t standard |

| Where to Buy | Directly from fund companies (MOS, SBI, HDFC, ICICI, etc.) — or buy from any trusted broker. | Through any brokerage account; can hold multiple fund companies’ ETFs in one place |

| Dividend Reinvestment | Seamless and automatic | Depends on broker — many offer DRIPs, but some don’t; can have delays |

| Best For | Best for passive investors, “set it and forget it”, | Investors who want trading flexibility and price control during the day. |

Common Myths and Misconceptions between investors about ETFs and Index Funds.

Common Myths and Misconceptions between investors about ETFs and Index Funds.

Most of the investors have misconceptions about these topics, you should be aware of these myths so you can make proper decisions and make investments.

1: ETFs Always Have Lower Fees Than Index Funds

It can be true, but not always. While many ETFs have very low expense ratios, some specialized or actively-managed ETFs charge 0.50% or more. Similarly, many index funds now offer expense ratios as low as 0.04% to 0.10%.

Always compare the specific expense ratios of the funds you’re considering, regardless of whether they’re ETFs or index funds.

2: ETFs Are Riskier Than Index Funds

The structure (ETF vs. index fund) doesn’t change the fundamental risk. An ETF and an index fund tracking the same index have essentially the same risk level. If both track the Nifty 50, both have the same risk exposure to those 50 companies.

3: You Need to Actively Trade ETFs

Absoultely no, just because you can trade ETFs throughout the day from exchange doesn’t mean you should. Most successful ETF investors buy and hold for years or decades, exactly like index fund investors. infact Etfs are best option for new investor who dont have expertise in thie markets.

The trading flexibility is there if you want it, but long-term investors typically ignore it.

4: Index Funds seemes like Old investment style; ETFs Are the Future

Both have their place. Index funds have existed since the 1970s and continue to manage trillions of dollars very successfully. ETFs are newer (created in the 1990s) and have grown rapidly, but that doesn’t make index funds obsolete.

Choose based on what works for your situation, not based on what’s “trendy.”

Which One is best for you or suitable for you?

Which One is best for you or suitable for you?

Here’s my honest advice based on different investor situations:

Choose Index Funds If:

You’re a beginner who wants the simplest possible experience. You plan to invest a fixed amount automatically every month and never want to think about it. You’re investing in a taxable account, but your fund company offers tax-efficient index funds. You prefer dealing directly with one fund company for all your investments. You want seamless automatic dividend reinvestment with zero effort.

Index funds are perfect for the “set it and forget it” investor who values simplicity and automation above everything else.

Choose ETFs If:

You can choose ETFs if you are new to the market. You’re comfortable using a brokerage account. You want the flexibility to buy or sell during market hours if needed. You’re investing across multiple fund companies and want everything in one brokerage account.

ETFs are great for investors who want flexibility and don’t mind a slightly more hands-on approach.

The Mistakes to Avoid as an investor

The Mistakes to Avoid as an investor

Overthinking the Choice

Analysis paralysis is real. Some beginners spend weeks agonizing over whether to choose an ETF or index fund, then never actually invest. Don’t let perfect be the enemy of good, so pick one and start investing. You can always adjust later.

Chasing short-term or past Performance

Don’t choose based on which one performed better last year or the last 5 years. If they track the same index, any performance difference is temporary and meaningless. Or always remember, past performance doesn’t guarantee future returns.

Forgetting About Costs in Your Excitement About ETFs

ETFs seem exciting because you can trade them. But trading costs money (through commissions or spreads) and triggers taxes. For most investors, the less you trade, the better you do. But if you are a trader, it’s a whole different thing.

Investing Too Conservatively Because You’re Confused

Some beginners, confused about the difference, end up not investing at all or putting money in a savings account earning 1%. Inflation is eating your purchasing power. Even an imperfect investment decision is usually better than no decision.

Advanced Considerations

Advanced Considerations

Once you’re comfortable with basic investing, here are some more advanced factors:

Portfolio Rebalancing: Both ETFs and index funds can be rebalanced, but the process differs slightly. With index funds, you can typically exchange between funds within the same family without triggering fees. With ETFs, you’ll need to sell one and buy another, which might trigger taxes in taxable accounts.

International Investing: If you want exposure to international markets, both ETFs and index funds offer options. ETFs sometimes provide access to more specific markets or regions that might not have index fund equivalents. AMC(Asset Management Companies) also runs ETFs that invests in foreign countries’ stocks. You can invest in them.

Sector-Specific Exposure: If you want to overweight a particular sector (like technology or healthcare), ETFs offer more variety than index funds. However, for beginners, broad market exposure is usually better than trying to pick winning sectors.

Bond Funds: Everything we’ve discussed applies to bond index funds and bond ETFs too. The same principles hold—low costs, passive management, diversification.

The Conclusion

ETFs and index funds are both excellent investment vehicles for building long-term wealth. They’re far more similar than they are different.

Index funds offer simplicity, seamless automation, and a completely hands-off experience. They’re perfect for investors who want to set up automatic contributions and never think about their investments again.

ETFs offer flexibility, lower minimum capital, slightly better tax efficiency, and the ability to trade during market hours. They’re ideal for investors who are comfortable with brokerage accounts and want more control over its inevstments.

Invest in index funds in tax-advantaged retirement accounts where automation is valuable and tax efficiency doesn’t matter.

The structure you choose—ETF or index fund—is far less important than simply getting started and sticking with it.

The best investment is the one you’ll actually make and hold onto for the long term. Whether that’s an ETF or an index fund, both will serve you well if you let time and compounding work their magic.

Frequently Asked Question.

Can I lose money with index funds or ETFs?

Yes, both can lose money in the short term because they invest in stocks or bonds, which fluctuate in value. However, historically, broad market indexes have always recovered and grown over long periods (15-20+ years). The risk of loss decreases dramatically the longer you hold.

Which is better for retirement investing?

For most retirement accounts like 401(k)s or IRAs, it doesn’t matter much. Choose whichever has lower fees. If your 401(k) offers index funds, use those. If you have an IRA with a brokerage, either works fine.

Can I convert an index fund to an ETF or vice versa?

Some fund companies like Vanguard allow you to convert index fund shares to ETF shares of the same fund without triggering taxes. But generally, switching from one to the other means selling one and buying the other, which creates a taxable event in taxable accounts.

Do ETFs or index funds pay better dividends?

Neither pays better dividends. If they track the same index, they receive the same dividends from the underlying companies and pass them through to investors. The dividend yield will be nearly identical.

Are ETFs or index funds better during a market crash?

Neither offers protection during a crash—both will decline with the market. However, ETFs allow you to sell immediately during market hours if you choose, while index fund orders execute at day’s end. That said, selling during a crash is usually a mistake regardless of which you own.

Is it smart to have both ETFs and index funds?

Absolutely. Many investors use index funds in retirement accounts for automatic investing and ETFs in taxable accounts for tax efficiency. There’s no requirement to choose only one type across your entire portfolio.

My name is Prabhat Mehta, and I’m from Jharkhand, India. I’m a CFA Level 1 candidate and currently pursuing a Bachelor of Commerce (B.Com) with a specific academic focus on financial analysis, corporate finance, and investment fundamentals.

I have a passion for studying and analysing financial markets, company valuation, and fundamental analysis. I feel immense joy and energy whenever I engage in these activities. I write articles to explain complex financial concepts simply and clearly, providing practical explanations to help investors avoid common mistakes and make better financial decisions.

Most retail investors struggle not because of a lack of funds, but because of a lack of clear financial understanding—they don’t know what investing is, how to get started, or how to select undervalued stocks with good growth potential. My work is to focus on solving those problems.

Investing isn’t just about investing in a single asset. I believe investing should be logical, disciplined, and knowledge-driven rather than emotional. Through continuous learning and real-world analysis, my aim is to foster sound financial thinking and share information that truly helps investors grow with confidence over time.