If you work in the finance domain or are interested in the world of financial investing, you may have asked yourself: “What is Yield to Maturity?” Why and how do some bonds with the same interest rate offer completely different returns?”

Most investors look at the interest rate (coupon rate) and assume that’s exactly what they’ll get from the bond. They might see a 5% bond and think, “Great, I’ll get a 5% return.” But in the ever-changing world of finance, it’s not that simple.

In this comprehensive guide, we’ll explain the meaning of YTM (Yield to Maturity) and explain everything you need to know about YTM in simple terms.

Understanding Yield to Maturity in Simple Words

In simple terms, Yield to Maturity is simply the total, true annual return you will make on a bond if you buy it today at its current market price, collect every single interest payment, and hold onto it until the day the bond expires (maturity date).

For calculating yield to maturity, you need some data:

1. The interest payments you receive.

2. The difference between what you paid for the bond and what you get back at the end from the bond.

3. The time it takes to get your money back.

understand with some examples :

Purchasing a House for Investment

Imagine you are buying a rental property. You collect monthly rent from your tenants (representing a bond’s regular interest payments). However, your overall return on investment isn’t just the rent. It also depends on whether you bought the house for a bargain or overpaid for it, and what it will be worth when you finally sell it. YTM combines the “rent” and the “property value change” into one single annual percentage.

Another Example: Fixed Deposits Versus Bonds

When you put money in a bank fixed deposit, you put in $1,000, get 4% a year, and get your $1,000 back. It never changes. Bonds, however, can be bought from other investors. You might buy a $1,000 par value bond for $900. Now, you are getting the interest payments *and* an extra $100 when the bond finishes. YTM combines both of these income streams into one percentage. (Do not compare bonds from fixed income securities for investment purposes)

YTM Formula and calculation :

The exact YTM formula requires a financial calculator because it involves trial and error. But there is a simple approximation formula that gives you a close enough answer:

YTM = [ C + (F – P) / n ] / [ (F + P) / 2 ]

Where:

- C = Annual coupon payment (in ₹)

- F = Face value of the bond (usually ₹1,000)

- P = Price you paid for the bond

- n = Number of years until maturity

Step-by-Step Calculation with an Indian Example

Let’s say you are looking at an REC Limited bond (a popular PSU bond in India) with these details:

- Face Value (F): ₹1,000

- Annual Coupon (C): ₹70 (7% coupon)

- Market Price (P): ₹920 (buying at a discount)

- Years to Maturity (n): 5 years

Step 1 — Numerator (Average Annual Profit)

₹70 + (₹1,000 − ₹920) / 5 = ₹70 + ₹16 = ₹86

Step 2 — Denominator (Average Capital)

(₹1,000 + ₹920) / 2 = ₹960

Step 3 — YTM

₹86 / ₹960 = 8.96%

Even though the coupon rate is 7%, your actual YTM is nearly 9% because you bought the bond below its face value.

Why Yield to Maturity Matters to Investors?

Why should you care about YTM? Why not just look at the interest rate and call it a day?

Here is why YTM is important for investors:

Measuring True Bond Returns: The interest rate only tells you the cash flow. YTM tells you the actual wealth you are building. It is the true measure of profitability.

Comparing Different Bonds: How do you choose between a bond paying 3% selling at a steep discount, and a bond paying 6% selling at a premium? It is like comparing apples to oranges. YTM turns them both into a single percentage, allowing for a perfect apples-to-apples comparison.

Making Smarter Investment Decisions: Whether you are buying corporate bonds or government bonds, YTM helps you see through the marketing noise to find where the real value lies.

Retirement Planning: Retirees rely on fixed income. Knowing your precise YTM allows you to project exactly how much your portfolio will grow over the next decade.

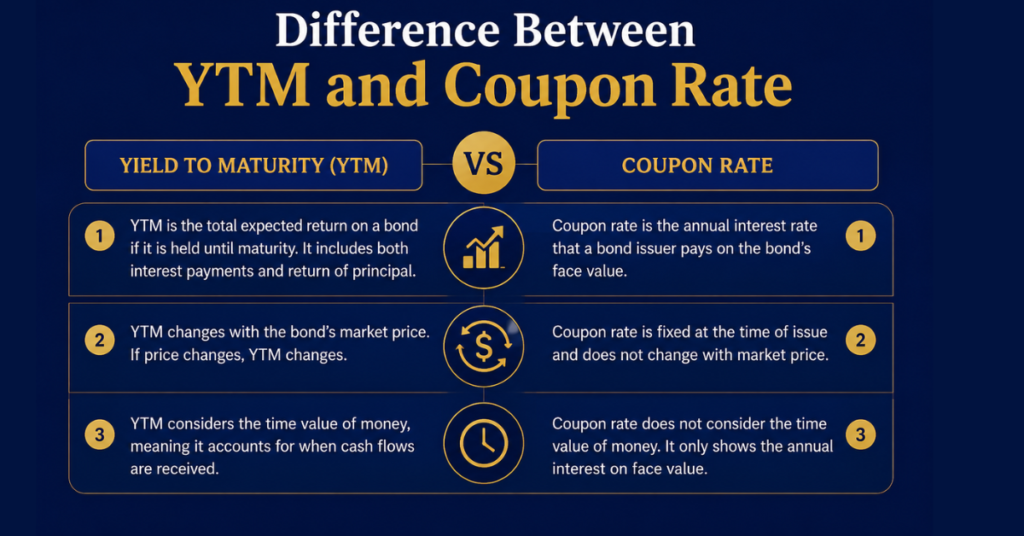

The difference between YTM and Coupon Rate?

| Features | Coupon Rate | YTM |

| What it is | Fixed interest rate (coupon payment) on face value | It shows the Total annual return, including price difference |

| Does it change? | No, fixed for the life of the bond | Yes, it changes every time the price changes. |

| Best used for | Knowing your interest cash flow | Comparing true returns across multiple bonds. |

Simple rule: If you buy a bond at exactly its face value, then the coupon rate = YTM. The only difference when you buy above or below face value.

When Bond Price and YTM Move Together

The most important rule in bond investing:

Bond Price goes DOWN → YTM goes UP

Bond Price goes UP → YTM goes DOWN

This is called the inverse relationship between price and yield. Here is why it happens.

For better understanding, let’s say you buy an NHPC bond that was paying 6% interest when it was issued. A year later, the RBI raises interest rates, and new bonds are now being issued at 8%. After this increase, no one wants your 6% bond at full price.

So investors start selling the bond, and the increased selling pressure causes the bond price to fall. The person who bought it at the lower price is now actually getting a higher return—so the YTM increases, even though the coupon rate remains at 6%. This is why there’s always an inverse relationship between bond price and bond YTM.

What are the circumstances that most impact your YTM?

YTM (Yield to Maturity) changes based on real-world events. These are the main factors that most impact YTM:

• RBI Repo Rate: When the RBI/Central Bank raises rates, new bonds offer higher coupons. The value of older bonds decreases, increasing their YTM. When the RBI lowers rates, the opposite occurs.

• Inflation: High inflation in the country is also a factor, as investors demand higher YTMs to maintain purchasing power.

• Credit Risk: A AAA-rated NHAI bond will have a lower YTM than a BBB-rated company bond. Riskier bonds require higher payments due to their credit risk (default risk).

• Demand and Supply: If many investors want a particular bond, the price rises, and YTM automatically falls due to demand and supply.

Limitations of YTM:

Real risks that show that YTM is not a guarantee:

Reinvestment Risk: YTM assumes you reinvest every coupon payment at the same YTM rate. In reality, rates keep changing, so your actual return will be slightly different. This is the biggest risk.

Default Risk: If the company goes bankrupt (think DHFL in India), at this point in time, YTM becomes meaningless. Always check the bond rating before taking any investment-related decision.

Selling Early: If you sell before maturity, you get whatever the market price is that day — not the YTM you calculated when you bought.—

Common Mistakes Every Investor Makes: But you need to avoid

1. Chasing high YTM blindly: A 14% YTM on a corporate bond sounds great until the company defaults or goes bankrupt. High yield = high risk. Always check the credit rating and reasons.

2. Looking only at coupon rate: Never evaluate a bond just by its coupon. A 9% coupon bond selling at ₹1,200 might have a YTM of only 6%.

3. Ignoring call features: Some bonds let the issuer repay early (callable bonds). If rates fall, the issuer will call the bond, and you lose your high-yielding investment. Always check “Yield to Call” alongside YTM.

4. Locking money for too long: Buying a 15-year bond when you might need the money in 3 years is a trap. Match maturity with your financial goal.

5. Panic selling when price drops: Bond prices fall when rates rise — that is normal. If you hold to maturity, you still get your face value. Do not panic and sell at a loss.

How to use YTM for better comparison?

You do not need to calculate YTM manually. Every bond on platforms like Zerodha Coin, Grip Invest, Growwm, or ICICI Direct already shows the YTM on your portfolio. Your task is just to read and compare the data with your peers. Here is what to check:

• Is the YTM higher than current FD rates? If not, why take bond risk? Why not invest in Fd?

• Is the YTM much higher than similarly rated bonds? If yes, something is risky — find out what the fundamental research of the company deeply reveals, there is something that you don’t know.

• What is the credit rating? AAA is safest, AA is good, anything below BBB needs careful thought. and do not invest only based on high-yield junk bonds offers high yield.

• When does it mature? Does that match when you will need the money?

The Conclusion

Whenever you buy a bond, never stop at the coupon rate. The coupon payment/rate only tells you how much cash you receive each year. But YTM tells you your actual total return.

A 6% coupon bond at a discount can easily beat a 9% coupon bond bought at a premium — and YTM is the one number that shows you this truth.

Use it to compare, not just to look impressed by a high coupon number. The investor who understands YTM will always make smarter decisions than the one who does not. This is only the surface-level basic information about YTM; for more knowledge, consider deep research.

Frequently Asked Question

Is a higher YTM always better?

No. Higher YTM almost always means higher risk. A 12% YTM on an unknown company bond might look attractive, but the market is pricing in a real chance of default. Compare YTM only among bonds with similar credit ratings.

Can YTM be negative?

Yes, though it is very rare in India. It means you are guaranteed to get back less than you paid. It happens when bond prices are bid up so high that the math flips. Practically, you will not see this in the Indian retail bond market.

What if I sell the bond before maturity?

Your YTM no longer applies. Your return depends on the market price on the day you sell. This is called your Holding Period Return and can be higher or lower than the original YTM.

Do I have to calculate YTM manually?

Never. All bond platforms in India show YTM automatically. You just need to understand what it means and how to compare it.

Is YTM the same as yield?

Not exactly. “Yield” is a broad term. YTM is a specific type of yield that assumes you hold the bond until it matures. There is also Current Yield (annual coupon ÷ market price) and Yield to Call (if the bond is callable).

My name is Prabhat Mehta, and I’m from Jharkhand, India. I’m a CFA Level 1 candidate and currently pursuing a Bachelor of Commerce (B.Com) with a specific academic focus on financial analysis, corporate finance, and investment fundamentals.

I have a passion for studying and analysing financial markets, company valuation, and fundamental analysis. I feel immense joy and energy whenever I engage in these activities. I write articles to explain complex financial concepts simply and clearly, providing practical explanations to help investors avoid common mistakes and make better financial decisions.

Most retail investors struggle not because of a lack of funds, but because of a lack of clear financial understanding—they don’t know what investing is, how to get started, or how to select undervalued stocks with good growth potential. My work is to focus on solving those problems.

Investing isn’t just about investing in a single asset. I believe investing should be logical, disciplined, and knowledge-driven rather than emotional. Through continuous learning and real-world analysis, my aim is to foster sound financial thinking and share information that truly helps investors grow with confidence over time.