Table of Contents

In the world of investment and finance, terms such as “fixed-income instruments (bonds),” “coupon rate,” and “yield to maturity” can seem quite difficult to new investors.

However, in reality, bonds are among the simplest, most reliable, and most effective investment vehicles available to the general public. Every year, millions of Indians deposit their hard-earned money into Fixed Deposits (FDs)—and bonds function in much the same way; the only difference is that they often offer you better returns, greater flexibility, and, at times, tax exemptions as well.

In this article, we will explore in detail what a bond is, how it works, the various types of bonds available in India, the risks associated with investing in bonds, how to purchase bonds, and whether bonds constitute the right investment choice for you.

| 💡 Quick: If you can understand how lending money to a friend works, you can understand bonds. It’s that simple — and we’ll prove it. |

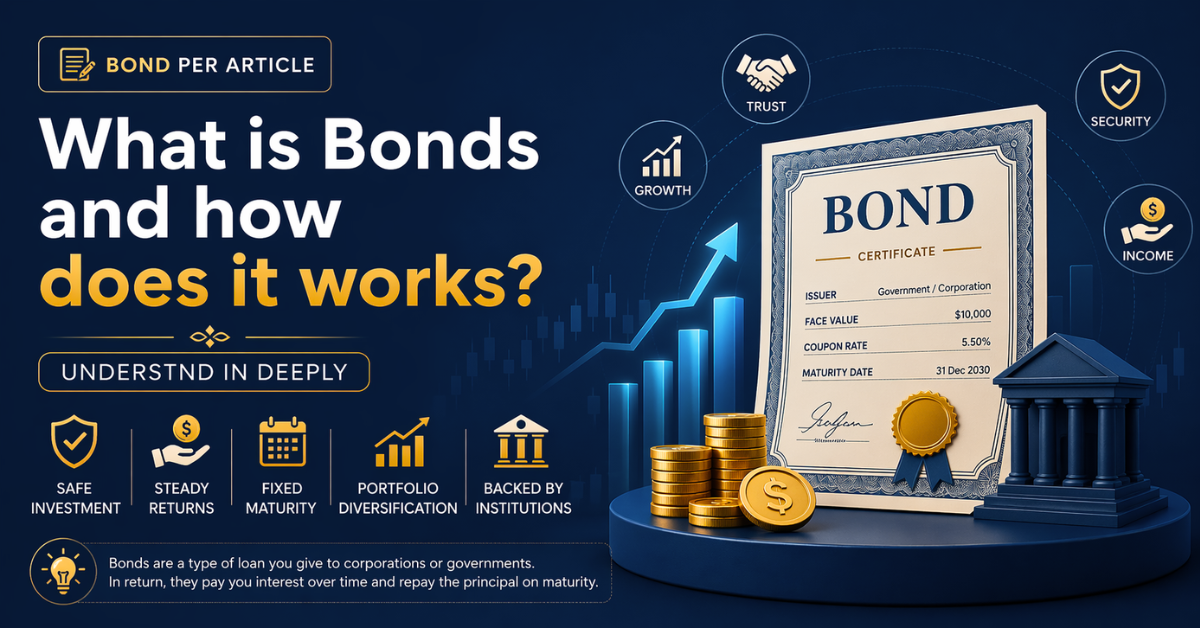

1. What is a Bond?

A bond is known as a fixed-income instrument. In simple terms, a bond is a loan that you give to a company or the government. In return, they promise to pay you a fixed interest rate (coupon) at regular intervals — monthly, quarterly, or annually — and return your original amount (principal) at the end of a fixed period (maturity date).

For example, your friend Ramesh wants to start a small business. He needs Rs. 1 lakh to buy equipment. He comes to you and says, “Lend me Rs. 1 lakh. I will pay you 8% interest every year for 5 years, and at the end of 5 years, I will return your Rs. 1 lakh.” You agree, you write it down, and it becomes a legal agreement.

Now, imagine the same thing — but instead of your friend Ramesh, it’s a giant company like Tata Motors or even the Indian Government that needs money.

| 📌 In Simple Words: Bond = You lend money → They pay you interest regularly → They return your money at the end. |

The Core Elements of Bond

Every single bond in the world — whether it’s a Government of India bond or a bond issued by Reliance Industries or Raju Electronics — has three basic components:

| Terms | What It Means | Example |

| Principal / Face Value | The original amount you invest — the money you lend to them | Rs. 1,000 (common face value in India) |

| Coupon Rate | The interest rate the issuer pays you every year | 7.5% per year on your Rs. 1,000 |

| Maturity Date | The date when they return your principal to you | 5/10/20 years from today |

So if you buy a bond with a face value of Rs. 1,000, a coupon rate of 8%, and a maturity of 10 years — here’s what happens with your capital:

- You pay Rs. 1,000 today

- You receive Rs. 80 every year for 10 years (8% of Rs. 1,000 = Rs. 80)

- At the end of Year 10, you get your Rs. 1,000 back

- Total you earned: Rs. 80 x 10 = Rs. 800 in interest + Rs. 1,000 principal back

2. How Does a Bond Actually Work? (Step-by-Step)

Let’s understand the entire life cycle of a bond using a real-world example. Suppose the Power Finance Corporation (PFC) — a Government of India enterprise — needs Rs. 10,000 crore to fund new power plants across the country. Here is the process

Step 1: The Issuer Decides to Issue a Bond

PFC goes to SEBI (Securities and Exchange Board of India) and says, “We want to borrow money from the public by issuing bonds.” They file the necessary paperwork, decide on the terms — the interest rate, the tenure (say 10 years), and the face value (say Rs. 1,000 per bond).

Step 2: The Bond Is Offered to Investors (Primary Market)

Now, PFC opens a public issue — similar to how a company issues an IPO for its stock. You can apply through your broker, a bank, or platforms. Millions of investors subscribe. If you invest Rs. 10,000, you buy 10 bonds (at Rs. 1,000 each) for 10 years.

Step 3: Receiving Interest Payments

PFC offers 7.8% annually. On Rs. 10,000 invested, you’ll receive Rs. 780 every year. Depending on the bond terms, this might come to you every 6 months (Rs. 390 twice a year) or once a year. The payment hits your bank account directly.

Step 4: You Can Trade It (Secondary Market)

you don’t have to hold a bond until maturity. Bonds are listed on the NSE and BSE, just like stocks. So if you need money urgently after 2 years, you can sell your bond to someone else at the prevailing market price.

Step 5: Maturity Date — You Get Your capital Back

On the maturity date — after10 years from the issue date — PFC automatically credits the face value (Rs. 1,000 per bond) back to your account. Your bond expires, and the relationship ends. You walk away with all your original capital plus all the interest you collected along the way.

| 🇮🇳 Real Example: REC Limited (Rural Electrification Corporation) issued bonds in 2024 with a coupon of 7.74% p.a. for 10 years. Face value: Rs. 1,000. An investor who bought 100 bonds (Rs. 1 lakh) would earn Rs. 7,740 every year for 10 years — that’s Rs. 77,400 in total interest, plus getting their Rs. 1 lakh back. Better than most FDs at the time. |

3. Bond Terminology Glossary — Quick Reference

Here are the most important terminologies related to bond, in simple language:

| Term | Plain English Meaning |

| Face Value / Par Value | The original loan amount — usually Rs. 1,000 in India |

| Coupon Rate | The interest rate (e.g., 8% per year) you will receive from the borrower. |

| Coupon Payment | The actual rupee interest you receive (8% of Rs. 1,000 = Rs. 80/year) |

| Maturity Date | The date you get your original money back (principal) |

| Yield to Maturity (YTM) | Your actual total return if you hold the bond till the end. |

| Credit Rating | A score (AAA to D) given by CRISIL/ICRA for how safe the bond is. |

| Primary Market | Buying a brand-new bond directly from the issuer in the primary market |

| Secondary Market | Buying an existing bond from another investor on NSE/BSE |

| Duration | How sensitive is your bond’s price to interest rate changes? |

| Callable Bond | A bond that the issuer can repay early (before maturity). Callable bonds give the issuer the right to buy back the bonds before maturity. |

| Puttable Bonds | Puttable Bonds give investors the right to sell the bond back before maturity. |

| Zero-Coupon Bond | No regular interest; sold at a discount and redeemed at face value |

| NCD | Non-Convertible Debenture — a type of corporate bond in India |

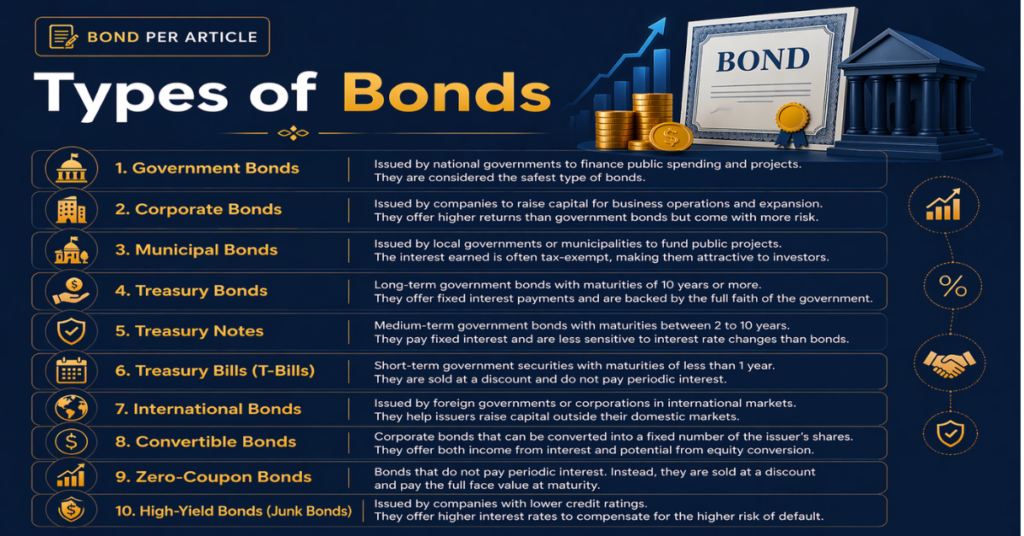

4. Types of Bonds in India

Not all bonds are the same. Different types serve different purposes and come with different risk levels. Here’s a clear breakdown of the most common ones you’ll encounter in India:

A. Government Securities (G-Secs)

These are bonds issued by the Central Government of India through the Reserve Bank of India (RBI). They are considered the SAFEST investment in the country because they are backed by the Government of India — the entity that can literally print money and pay you if needed.

- Issuer: Government of India (via RBI)

- Typical Yield: 6.5% to 7.5% per year (2026 rates)

- Tenure: Can range from 91 days (T-Bills) to 40 years

- How to Buy: RBI Retail Direct portal (free, no broker needed)

| 💡 Best For: these types of bonds are suitable for conservative investors who want safety and a guaranteed return — like keeping money in a government vault that also pays interest. |

B. State Development Loans (SDLs)

These bonds are issued by State Governments — like the Government of Maharashtra, Tamil Nadu, or Uttar Pradesh. They are almost as safe as Central Government bonds but offer slightly higher interest rates (typically 0.25–0.50% more than G-Secs) because state finances can sometimes be less stable than the Centre’s.

C. PSU Bonds (Public Sector Undertaking Bonds)

These are issued by government-owned companies like NTPC, IRFC (Indian Railway Finance Corporation), NHAI, REC, and PFC. They are backed (though not fully guaranteed) by the government and carry very high credit ratings — usually AAA.

| 🇮🇳 Real Example: IRFC (Indian Railway Finance Corporation) issues bonds to fund railway infrastructure. Since the Indian Railways generates massive revenue, these bonds are ultra-safe and offer returns of around 7.3-7.8% — significantly better than the average FD. |

D. Corporate Bonds

These types of bonds are issued by private companies — Reliance Industries, HDFC, Bajaj Finance, Tata Capital, etc. They offer higher returns than government bonds because they carry more credit risk. A corporate bond might give you 9–12% if the company is creditworthy but smaller, versus 7–8% for a large, established conglomerate.

5. Difference Between Bonds vs. Fixed Deposits:

Most common question among investors. Most people are familiar with Fixed Deposits (FDs) in SBI or HDFC Bank. So why bother with bonds? Let’s compare them head-to-head:

| Features | Fixed Deposit (FD) | Bond |

| Who Offers It? | Banks & NBFCs | Govt, Companies, PSUs |

| Returns (approx.) | 6.5 – 7.5% (2026) | 7 – 12%+ depending on type and credit risk |

| Safety | Up to Rs. 5 lakh DICGC insured | Sovereign or company-backed (ABS or MBS) |

| Liquidity | You can redeem your investments with a penalty. | Trade on NSE/BSE anytime, no penalty for redemption, only brokerage |

| Taxes | Interest taxed as income | Short-term or long-term taxes are applied here. Some bonds are TAX-FREE. |

| Tenure | 7 days to 10 years | 1 month to 40 years |

| Minimum Investment | Rs. 1,000 typically | Rs. 1,000 (face value) |

| Where to Buy | Bank branch or app | Online via broker/platform |

For investing, Bonds are generally better than FDs in terms of returns and flexibility. The only catch is that FDs have the DICGC insurance guarantee up to Rs. 5 lakh per bank, which provides a safety net for small savers. But for amounts above Rs. 5 lakh, high-quality credit ratings bonds are often a smarter choice.

6. How Bond Prices and Interest Rates Are Connected

Once you understand the connection between bonds and interest rates, you will also understand bond markets. Here is the Golden Rule of Bonds:

🔑 The Golden Rule of Bonds: When interest rates rise → bond prices fall. When interest rates fall → bond prices rise. They always move in opposite directions.

Why? Let’s take an example. A company is offering an 8% coupon on its bonds. Now, suppose the RBI raises interest rates, and new, higher-rated bonds begin offering a 10% coupon. Suddenly, your 8% bond starts to look less attractive. Why would anyone buy that old bond—which offers a coupon of only 8%—when they can receive a 10% coupon annually from a new bond?

No one buys that old bond; consequently, most investors begin selling their old bonds to invest in the new ones. Therefore, due to this increased selling pressure, the market price of your bond quickly drops below its face value.

Conversely, when the RBI lowers interest rates (as it is doing in 2025–2026), your old 8% bond becomes highly attractive, and its price rises to well above ₹1,000.

Tip: If you plan to hold a bond until its maturity, changes in interest rates will not affect you—you will always receive your fixed coupon payments and your principal amount back. Price fluctuations matter only if you intend to sell the bond before it reaches maturity

7. Risks involved with bond investing

Every investment carries some degree of risk; indeed, every type of investment comes with its own unique set of risks and rewards. Similarly, bonds are also subject to various risks, which are outlined below.

Risk 1: Credit Risk (Default Risk)

This refers to the risk that the company issuing the bond may go bankrupt and be unable to repay your invested capital. This is precisely why the interest offered on corporate bonds is higher than that on government bonds; this additional interest serves as compensation for the inherent credit risk.

Before investing, you should always verify the bond’s credit rating. CRISIL, ICRA, and CARE are India’s three primary credit rating agencies. An ‘AAA’ rating is considered the highest (and safest) rating a company can receive.

Risk 2: Interest Rate Risk

As mentioned above, when market interest rates rise, the value of your existing bonds tends to fall. If you are compelled to sell your bond before its maturity date, you may receive an amount lower than your initial investment. If you are a long-term investor, it is advisable—whenever possible—to hold onto your bonds until they reach maturity. Alternatively, if you anticipate that interest rates are likely to rise, consider investing in short-duration bonds.

Risk 3: Liquidity Risk

Not all bonds are actively traded on stock exchanges. Some bonds—particularly corporate bonds with a small issue size—may experience low trading volumes. This implies that if you wish to sell your bonds quickly, you may be unable to find a buyer, or, due to a lack of liquidity, you may be forced to sell the bonds at a discounted price.

Risk 4: Inflation Risk

If the inflation rate is 7% and your bond is also yielding a return of 7%, your *real return* is considered to be 0%. Your purchasing power* remains the same as it was before. This is known as ‘Inflation Risk’—to beat inflation over the long term, choose bonds that offer you higher ‘real yields.’

Risk 5: Reinvestment Risk

When a bond matures, or when you receive the interest payments (coupon payments) associated with it, you must reinvest that money elsewhere. If interest rates have fallen by that time, you will be forced to reinvest your funds at lower rates, known as ‘Reinvestment Risk.’

| Risk Type | Who It Affects Most | Severity | Solution |

| Credit Risk | Corporate bond investors | High | Check ratings (AAA/AA only) |

| Interest Rate Risk | Long-term bondholders | Medium | Hold till maturity |

| Liquidity Risk | Investors in small bonds | Medium | Stick to the listed bonds |

| Inflation Risk | All bond investors | Low-Medium | Mix with equity |

| Reinvestment Risk | Coupon receivers | Low | Laddering strategy |

8. Who Should Invest in Bonds?

Bonds are not just for old, retired people or conservative investors. Here’s a clear guide on who benefits from bonds:

Bonds Are Ideal or useful If You Are…

- For a retired investor—or one nearing retirement—who seeks a regular income stream without assuming the risks associated with the stock market, investing in government bonds is the optimal choice for living a stress-free life.

- For a high-income professional (such as a doctor, lawyer, or business owner) falling within the 30% tax bracket, tax-free bonds offer distinct advantages; furthermore, in terms of investment security, bonds are safer than equities.

- Individuals building an emergency fund who desire returns superior to those offered by a standard savings account can invest in medium-rated bonds to generate higher yields.

- Parents saving for a child’s education or wedding within a specific timeframe can also allocate funds to debt instruments, aligning their investment choices with their individual risk appetite and investment horizon.

- Investors seeking to rebalance a portfolio—currently heavily weighted toward stocks and cryptocurrencies—can diversify a portion of their holdings into bonds to mitigate overall portfolio risk.

Bonds may *not* be the right fit for you if…

- You are a young investor (under the age of 30) with a long investment horizon—in the long run, equities typically outperform bonds; therefore, you should allocate the majority of your capital to equities to maximise returns on your investment.

- You are an individual who may require immediate and sudden access to funds—in such instances, stocks or liquid funds offer greater liquidity and accessibility.

- You are an individual deeply concerned about inflation—in a high-inflationary environment, bonds often fail to preserve your purchasing power; moreover, even low interest rates can erode your purchasing power, effectively diminishing the real value of your money.

💡 The “100 Minus Age” Rule: A simple guideline: Invest (100 minus your age)% in equities, and the remainder in bonds or debt instruments. At age 30, allocate 70% to stocks and 30% to other asset classes.

10. Common Bond Investment Mistakes and How to Avoid Them

Some common mistakes that every investor learns from others’ mistakes are always cheaper than making them yourself. Here are the most common errors Indian bond investors make:

Mistake 1: Chasing High Yields Without Checking Credit Ratings

A bond offering a 15% yield looks very attractive—but why is it paying so much? Because the borrower is risky, possesses a low credit rating, and must compensate investors for that risk. Do not blindly invest in “high-yield” bonds; these bonds carry a higher probability of default.

Mistake 2: Not Understanding What You Are Buying

Some investors confuse individual bonds with bond mutual funds or mistake debentures for bonds. Before investing, always seek to understand: Who is the issuer? What is the credit rating? When is the maturity date? Is the interest taxable? Can I sell it before maturity? When investing, you must find the answers to these questions based on your own research.

Mistake 3: Putting All Your Money into a Single Bond

Even a highly-rated bond can default under certain specific circumstances. Diversify your investments across various issuers and bond types. Furthermore, diversify your portfolio with other asset classes that have a negative correlation with one another to maximise the benefits of diversification.

Mistake 4: Panicked Selling When Bond Prices Fall

New investors sometimes observe that the market value of their bonds has dropped (typically due to rising interest rates) and, in a panic, sell them at a loss. Remember: If you hold a bond until maturity, you will always receive its face value (original principal amount) back. If you plan to hold the bond until the very end, short-term price fluctuations are of no consequence to you.

The Conclusion

Bonds are not get-rich-quick instruments. They are steady, reliable, stable, and boring instruments — and that’s exactly what makes them more powerful than other asset classes.

In a world where stock markets can drop 40% in a matter of weeks (like during COVID in 2020), that’s why having a solid chunk of your portfolio in bonds provides stability, regular income, and peace of mind. The best investors in the world, like Warren Buffett, who built wealth slowly over decades, have always maintained a bond allocation.

For Indian investors specifically, the opportunity is even better. Tax-free bonds from PSUs, sovereign gold bonds from RBI, and the RBI Retail Direct platform have made it easier than ever to access high-quality bonds with zero commission. There’s really no reason NOT to have at least some bonds in your portfolio.

This article is for educational purposes only and does not constitute financial advice. Don’t invest in any asset based on tips. Consult a SEBI-registered financial advisor before making any investment decisions. All return figures are indicative and based on market conditions as of April 2026.

Unity Wealth Capital

My name is Prabhat Mehta, and I’m from Jharkhand, India. I’m a CFA Level 1 candidate and currently pursuing a Bachelor of Commerce (B.Com) with a specific academic focus on financial analysis, corporate finance, and investment fundamentals.

I have a passion for studying and analysing financial markets, company valuation, and fundamental analysis. I feel immense joy and energy whenever I engage in these activities. I write articles to explain complex financial concepts simply and clearly, providing practical explanations to help investors avoid common mistakes and make better financial decisions.

Most retail investors struggle not because of a lack of funds, but because of a lack of clear financial understanding—they don’t know what investing is, how to get started, or how to select undervalued stocks with good growth potential. My work is to focus on solving those problems.

Investing isn’t just about investing in a single asset. I believe investing should be logical, disciplined, and knowledge-driven rather than emotional. Through continuous learning and real-world analysis, my aim is to foster sound financial thinking and share information that truly helps investors grow with confidence over time.